You think we have a retirement crisis now? Just wait. The worst impact will be to the 20 somethings and 30 somethings, and it has nothing to do with the funding of Social Security (at least not directly. ) I can’t even comprehend my granddaughter’s (age 5) generation.

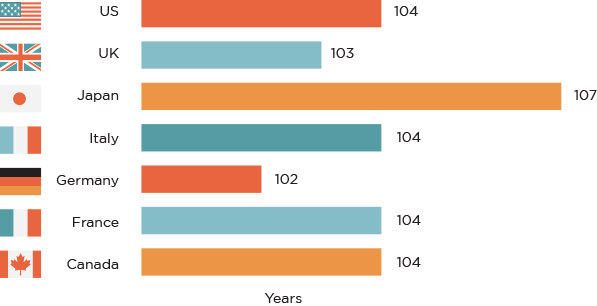

Consider the fact that for more than 200 years life expectancy in developed countries (You can argue that’s us) has increased 2 or 3 years every decade. Research complied by London School of Business professors Lynda Gratton (Management Practice) and Andrew Scott (Economics) show that most children born in the West (us) will live past their 100th birthday. Digest this graphic example:

Source: The Human Mortality Database: www.mortality.org

This is not climate change, folks: there is no debate allowed here.

While human longevity has been happening all along, we build our life stages and plan our retirements around the same assumptions our parents and grandparents did. Consider Social Security, conceived in 1935 when folks were expected to work until they retired at 65 years old, and died at age 67. Forget about anything like funding shortfalls in 2038. It was and is not equipped to deal with a 40 year retirement. NOTE: LIFE EXPECTANCY FOR CHILDREN BORN IN 1930 WAS 58 FOR MEN AND 62 FOR WOMEN. Chew on that in the context of the creation of the Social Security System.

Professors Scott and Gratton wrote a dramatic book (best book I ever read not written by Kurt Vonnegut) THE 100 YEAR LIFE, published June 2, 2016. Everyone should read it.

They state that the gift of longevity carries with it the curse of having to cope with it financially and socially. They call for “deep seated social change” to occur at the economic, social, political, business and individual level. From the book: “ We either can’t afford to retire at the age our parents did or will have to work for so long that our mental and physical fitness as well as our enthusiasm for life could suffer. Individuals, companies and governments all have a role to play in ensuring we structure our lives differently so we can make the most of a longer life.

For those in their 40’s-60’s they advise, “ Failure to innovate in response to a longer life will mean stresses and strains in your life as existing models are stretched uncomfortably over a 100 years”.

Most of us over 50 have been and are engrained in a three stage life: Education/training, career/work to accumulate, and retirement. This model will not and cannot hold. Professors Scott and Gratton predict we will have to move to a multi stage life, with perhaps several different career paths combined with pauses in between. They call it “individualized sequencing”. Retirement will be in your 80s, if at all.

For those in their 20s, think in terms of delayed saving for retirement, delayed accumulation careers, life experience enjoyment earlier and periodically along the way. This is not a rose-colored glasses wish; it is happening now. The 20 and 30 year olds currently are saving little now and enjoying life more. Now. They are embracing the multi stage life, maybe without even knowing it. While we old folks may cringe at this and say “how frivolous”, we are wrong. They are right.

Think of the business impacts. Human Resources needs to be refocused, careers have to be redefined, and the work-life balance made more flexible. Established corporations are built around the three stage life. Mark Zuckerberg and Elon Musk businesses, maybe not. After all, they’re innovators.

Governments need to move toward “lifetime measures rather than age specific policies. It has to address “pensions, education, relationships, families, households and career breaks”

Think of the impact on financial firms, insurance companies (think what Long Term Care insurance will have to look like), healthcare systems (do you think your premiums will go down ?), education institutions, recreation, retirement communities. The list is almost unending. It will have to be a massive total overhaul of the entire social infrastructure.

And what about personal finance in the days of the 100 Year Life?

My learned friend and colleague, Steve Barger says, “ No one is preparing today’s children or young adults for the probability that they will live to 100 or beyond. Living longer changes everything we do. RE: early education, extended work, recreation, health care, financial responsibilities, retirement targets, re-training for new skills and learning new information possibly at age 75.

The primary source for life preparedness (our educational institutions K – 16+) are so blinded by political correctness that they have completely ignored one of life’s critical survival skills: Managing one’s wealth.

There is not one college or university in this country that requires ‘personal financial proficiency’ in order to graduate. Where are our educational leaders? Nowhere to be found. How selfish and thoughtless. You should be ashamed.”

What does it mean for me? I won’t be around to see the upheaval.

What does it mean for my kids (38-42)? They’re thinking and saving and have already foregone traditional careers for more creative, holistic ones.

What does it mean for my grandchildren (5-14-16)? They WILL live that multi stage life, starting with “do it now” (whatever “it” is)

What does it mean for you? Our ancestors were artisans. Think about learning a trade, no matter what age.